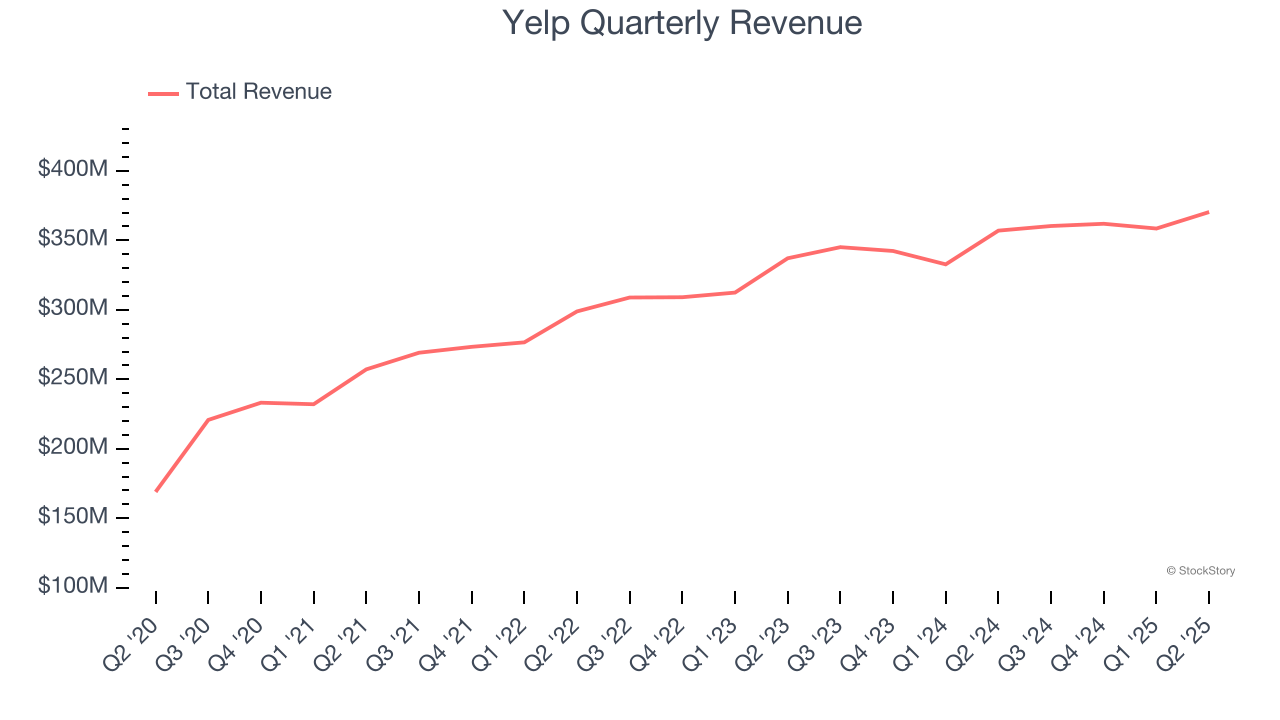

Local business platform Yelp (NYSE:YELP) announced better-than-expected revenue in Q2 CY2025, with sales up 3.7% year on year to $370.4 million. The company expects the full year’s revenue to be around $1.47 billion, close to analysts’ estimates. Its GAAP profit of $0.67 per share was 30.9% above analysts’ consensus estimates.

Is now the time to buy Yelp? Find out by accessing our full research report, it’s free.

Yelp (YELP) Q2 CY2025 Highlights:

- Revenue: $370.4 million vs analyst estimates of $365.4 million (3.7% year-on-year growth, 1.4% beat)

- EPS (GAAP): $0.67 vs analyst estimates of $0.51 (30.9% beat)

- Adjusted EBITDA: $100.5 million vs analyst estimates of $87.54 million (27.1% margin, 14.8% beat)

- The company reconfirmed its revenue guidance for the full year of $1.47 billion at the midpoint

- EBITDA guidance for the full year is $355 million at the midpoint, below analyst estimates of $359.3 million

- Operating Margin: 14.4%, up from 11.1% in the same quarter last year

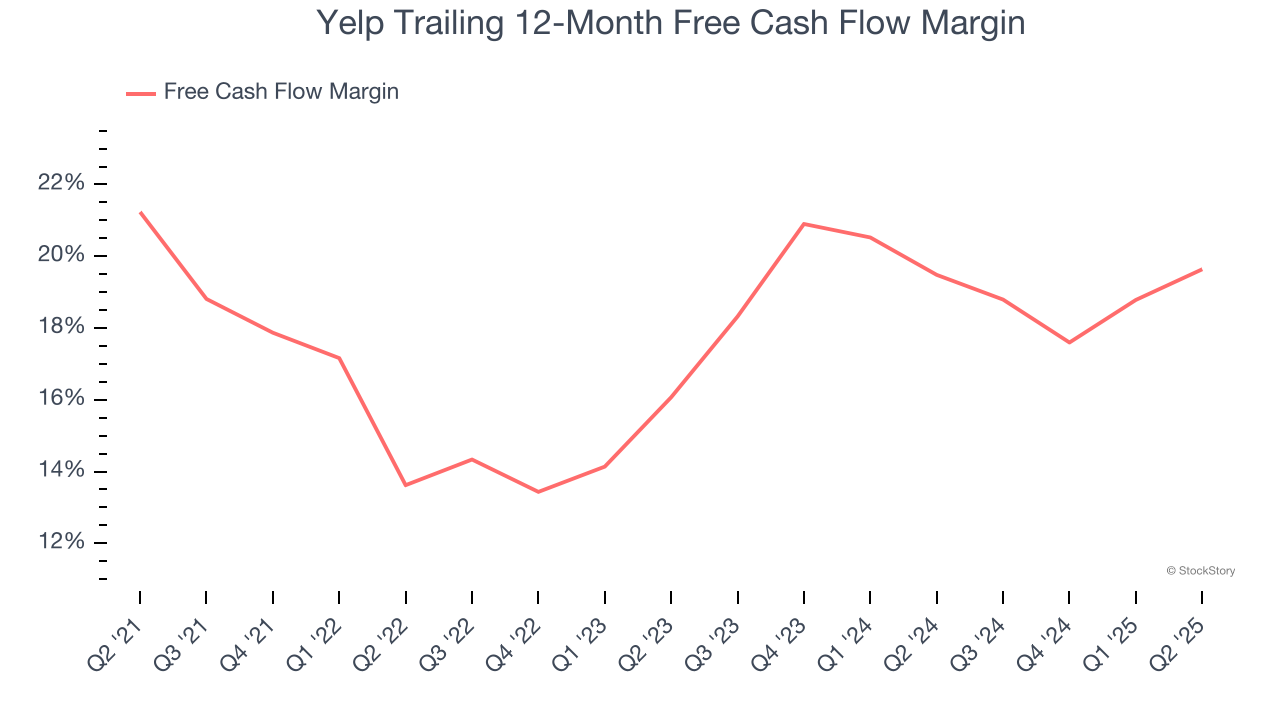

- Free Cash Flow Margin: 12.2%, down from 24.4% in the previous quarter

- Market Capitalization: $2.18 billion

“Our second quarter results reflect solid execution against our product-led strategy," said Jeremy Stoppelman, Yelp’s co-founder and chief executive officer.

Company Overview

Founded by PayPal alumni Jeremy Stoppelman and Russel Simmons, Yelp (NYSE:YELP) is an online platform that helps people discover local businesses through crowd-sourced reviews.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last three years, Yelp grew its sales at a mediocre 9.1% compounded annual growth rate. This wasn’t a great result compared to the rest of the consumer internet sector, but there are still things to like about Yelp.

This quarter, Yelp reported modest year-on-year revenue growth of 3.7% but beat Wall Street’s estimates by 1.4%.

Looking ahead, sell-side analysts expect revenue to grow 3.6% over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and implies its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Yelp has shown robust cash profitability, driven by its attractive business model that enables it to reinvest or return capital to investors while maintaining a cash cushion. The company’s free cash flow margin averaged 19.6% over the last two years, quite impressive for a consumer internet business.

Taking a step back, we can see that Yelp’s margin expanded by 6 percentage points over the last few years. This shows the company is heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

Yelp’s free cash flow clocked in at $45.01 million in Q2, equivalent to a 12.2% margin. This result was good as its margin was 3.7 percentage points higher than in the same quarter last year, building on its favorable historical trend.

Key Takeaways from Yelp’s Q2 Results

We were impressed by how significantly Yelp blew past analysts’ EBITDA expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. On the other hand, its full-year revenue guidance was in line and its full-year EBITDA guidance fell slightly short of Wall Street’s estimates. Zooming out, we think this was a mixed quarter. Investors were likely hoping for more, and shares traded down 3.8% to $32.99 immediately following the results.

Should you buy the stock or not? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.