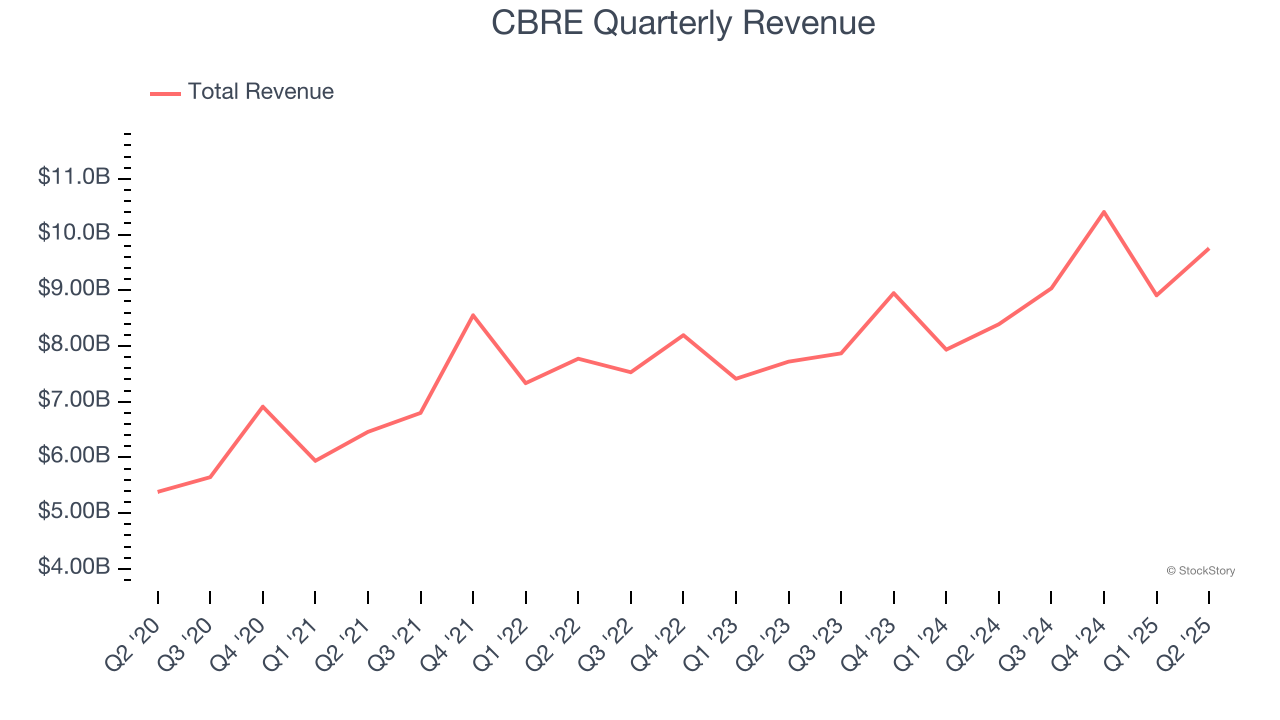

Commercial real estate firm CBRE (NYSE:CBRE) reported Q2 CY2025 results exceeding the market’s revenue expectations, with sales up 16.2% year on year to $9.75 billion. Its non-GAAP profit of $1.19 per share was 11.2% above analysts’ consensus estimates.

Is now the time to buy CBRE? Find out by accessing our full research report, it’s free.

CBRE (CBRE) Q2 CY2025 Highlights:

- Revenue: $9.75 billion vs analyst estimates of $9.35 billion (16.2% year-on-year growth, 4.3% beat)

- Adjusted EPS: $1.19 vs analyst estimates of $1.07 (11.2% beat)

- Adjusted EBITDA: $658 million vs analyst estimates of $636.5 million (6.7% margin, 3.4% beat)

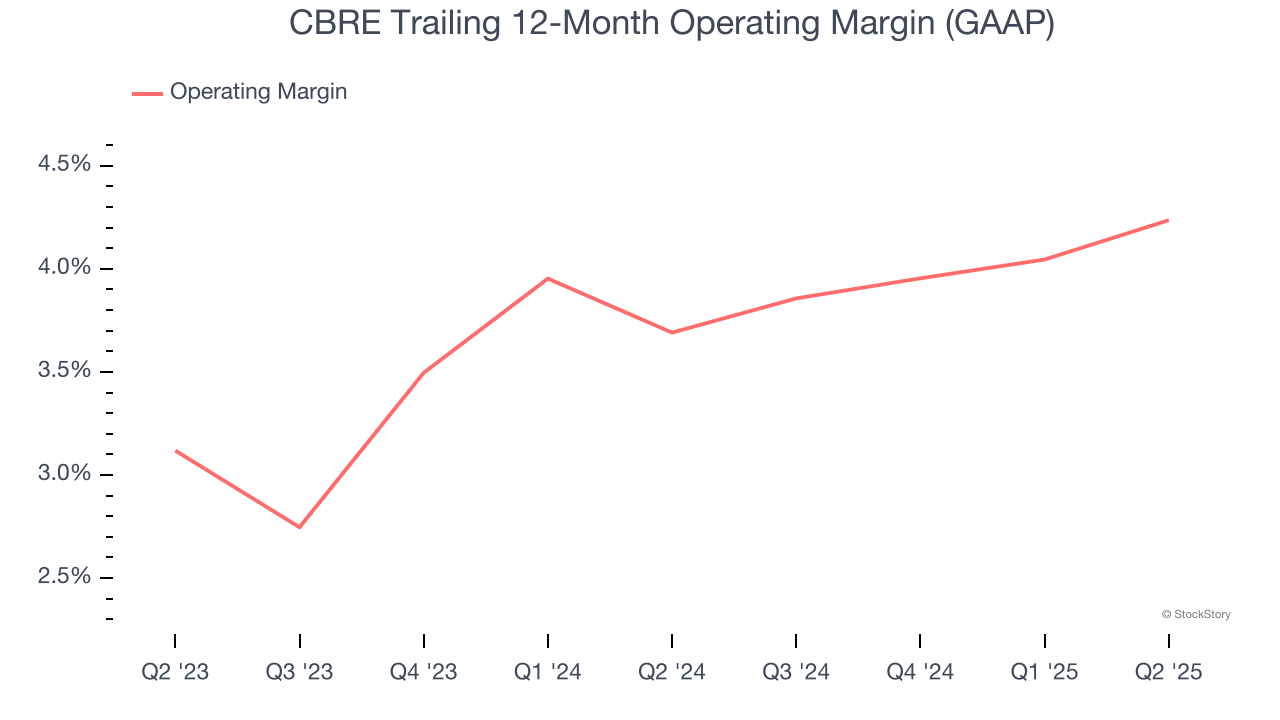

- Operating Margin: 3.8%, in line with the same quarter last year

- Free Cash Flow Margin: 6.2%, up from 2.6% in the same quarter last year

- Market Capitalization: $43.04 billion

“The strong momentum we exhibited to start the year continued in the second quarter. Despite uncertainty in the macro environment, occupier and investor clients largely proceeded with executing their plans,” said Bob Sulentic, CBRE’s chair and chief executive officer.

Company Overview

Established in 1906, CBRE (NYSE:CBRE) is one of the largest commercial real estate services firms in the world.

Revenue Growth

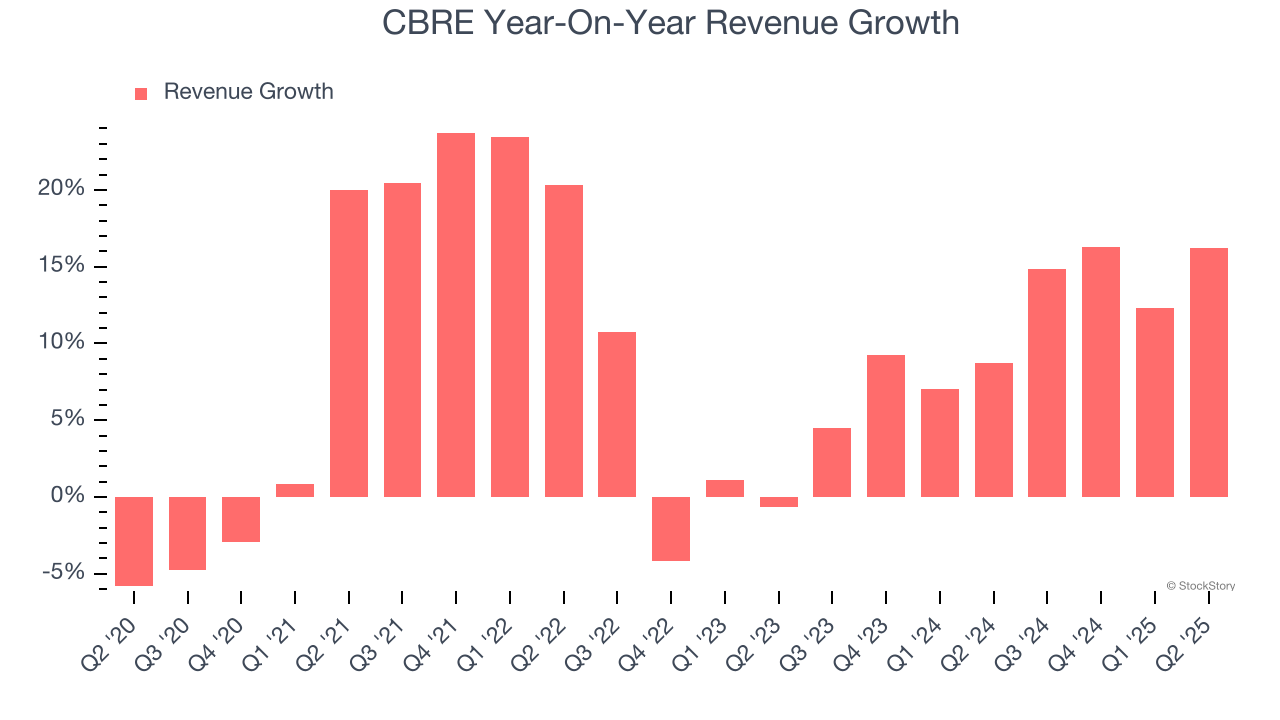

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, CBRE grew its sales at a tepid 9.4% compounded annual growth rate. This fell short of our benchmark for the consumer discretionary sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. CBRE’s annualized revenue growth of 11.1% over the last two years is above its five-year trend, but we were still disappointed by the results.

CBRE also breaks out the revenue for its most important segment, Advisory Services. Over the last two years, CBRE’s Advisory Services revenue (leasing, capital markets) averaged 6% year-on-year growth. This segment has lagged the company’s overall sales.

This quarter, CBRE reported year-on-year revenue growth of 16.2%, and its $9.75 billion of revenue exceeded Wall Street’s estimates by 4.3%.

Looking ahead, sell-side analysts expect revenue to grow 8.9% over the next 12 months, a slight deceleration versus the last two years. This projection doesn't excite us and implies its products and services will see some demand headwinds.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

CBRE’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 4% over the last two years. This profitability was lousy for a consumer discretionary business and caused by its suboptimal cost structure.

In Q2, CBRE generated an operating margin profit margin of 3.8%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

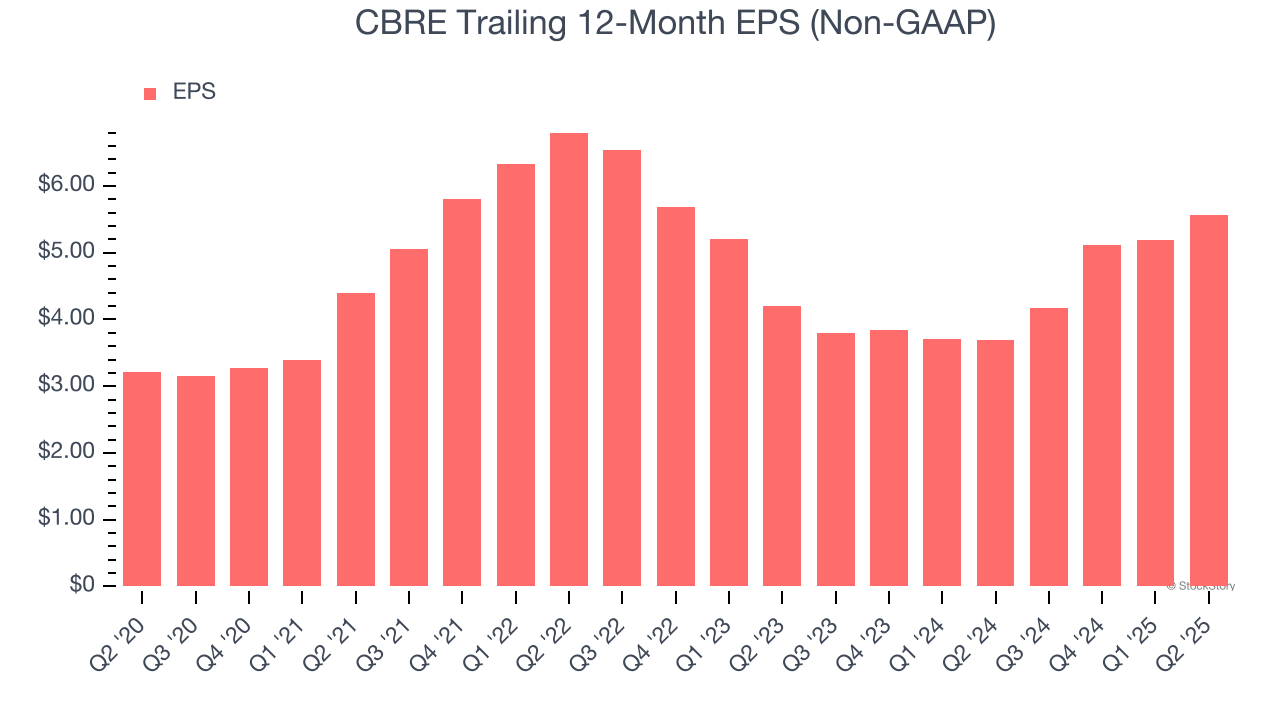

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

CBRE’s EPS grew at a decent 11.7% compounded annual growth rate over the last five years, higher than its 9.4% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

In Q2, CBRE reported EPS at $1.19, up from $0.81 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects CBRE’s full-year EPS of $5.57 to grow 15.5%.

Key Takeaways from CBRE’s Q2 Results

We enjoyed seeing CBRE beat analysts’ revenue expectations this quarter. We were also happy its EPS outperformed Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 1.4% to $148.67 immediately after reporting.

Indeed, CBRE had a rock-solid quarterly earnings result, but is this stock a good investment here? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.